As student demand tightens and affordability pressures rise, education strategist warns that scale without discipline may amplify risk rather than reduce it

United States, 18th Mar 2026 — The global education sector is entering a more competitive and economically complex phase as student demand tightens, affordability pressures increase, and capital continues to pursue aggressive expansion across international education markets.

Education strategist Elaina Cohen warns that many institutional growth strategies still reflect assumptions from a previous era—one characterized by expanding student mobility, rising middle classes, and steadily growing enrollment pipelines.

“Institutional brand alone is no longer sufficient,” Cohen said. “The global education market is becoming far more competitive, and strategies built for expansion cycles will not necessarily sustain institutions in the decade ahead.”

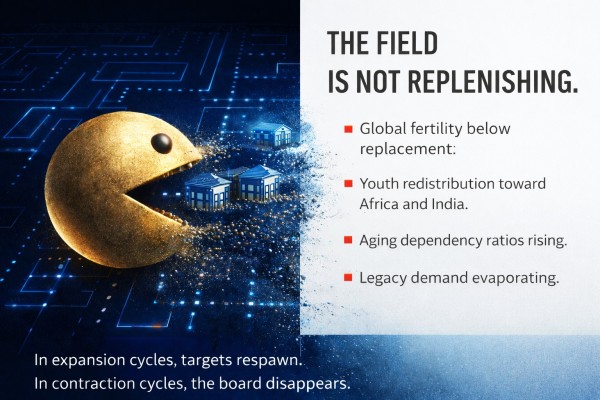

Across many developed economies, the number of school-age students is beginning to level off or decline as birth rates fall below replacement levels in numerous countries. While demographic change is only one factor shaping the education market, it is tightening the overall pipeline of potential students.

“We are all fishing in the same pool,” Cohen said. “And the pool is not expanding the way many institutions assumed it would.”

Yet capital continues to move aggressively through the sector.

Cohen argues that the pattern increasingly resembles a Pac-Man dynamic, with institutions rapidly acquiring schools across markets under the assumption that scale itself guarantees stability.

“That mindset can become a form of lazy fatalism,” she said. “It assumes that if you acquire enough schools, demand will somehow materialize.”

“But unlike the arcade game, the board does not refill.”

Demand Is Redistributing Rather Than Expanding

While traditional education markets across Europe, East Asia, and parts of North America face slowing student growth, youth populations are expanding elsewhere.

Sub-Saharan Africa and South Asia—particularly India—are poised to become some of the most significant education growth markets in the coming decades.

According to United Nations population projections, Sub-Saharan Africa’s population could nearly double by 2050, reaching more than 2 billion people. The region already has the youngest population globally, with a median age of roughly 19 years.

Countries including Nigeria, Ethiopia, Kenya, Tanzania, and Ghana are expected to experience substantial youth population growth.

India represents another powerful demographic center of gravity. With more than 250 million people between the ages of 15 and 24, the country holds the largest youth population in the world.

Economic growth is also reshaping these markets. Several African economies—including Rwanda, Kenya, Ghana, and Ethiopia—have recorded GDP growth rates frequently ranging between 5% and 8% annually, while India has maintained growth often exceeding 6% per year in recent years.

These trends are expanding demand for private schooling, international curricula, and global university pathways.

However, Cohen cautions that demographic expansion alone does not guarantee stable education markets.

“Demand ultimately follows purchasing power,” she said. “Population growth without income growth produces a very different market dynamic.”

When Capital Moves Faster Than Affordability

In many emerging markets, international school tuition can exceed several multiples of average household income. As a result, demand is often limited to expatriate communities or a narrow domestic elite.

This creates a structural tension between investor expectations and economic capacity.

“GDP growth headlines can be misleading,” Cohen said. “The real question is how quickly household income and middle-class purchasing power are expanding.”

Without that alignment, institutions expanding rapidly into emerging markets may encounter volatile enrollment cycles and persistent pricing pressure.

“Capital often moves faster than household income,” Cohen said. “When that happens, institutions end up competing for the same small segment of families.”

The Risk of Leap-Frog Investment

As global investors pursue growth opportunities in education, some institutions have adopted what Cohen describes as “leap-frog investment.”

Leap-frog investment occurs when premium schools are built or acquired in anticipation of future wealth expansion before the underlying middle class has fully developed.

“Infrastructure investment is essential,” Cohen said. “But leap-frogging the income curve can create fragile markets.”

If middle-class purchasing power expands more slowly than expected, institutions may face under-enrollment, heavy discounting, or persistent competition for a limited pool of affluent families.

The Limits of Tuition Inflation

For decades, many institutions relied on annual tuition increases as a predictable revenue strategy. In numerous private education markets, tuition has risen five to seven percent year over year for extended periods.

However, that model is becoming increasingly difficult to sustain.

Across many developed economies, household income growth has not kept pace with tuition inflation. In the United States, median household income has grown roughly three to four percent annually over the past decade, while private school and university tuition has often increased at significantly higher rates.

Rising costs for housing, healthcare, childcare, and transportation are also placing increasing pressure on family budgets.

“Tuition increases of seven percent year over year are simply not digestible for many families anymore,” Cohen said. “When pricing consistently outpaces income growth, institutions eventually reach a ceiling.”

Evidence of this pressure is already visible across the sector. Tuition discounting has expanded significantly, with average discount rates at U.S. private colleges now exceeding 50 percent for first-time students, according to enrollment industry reports.

“Increasing sticker price while expanding discounts creates the illusion of growth,” Cohen said. “But in many cases the net yield is deteriorating.”

Structural Misalignment in the Education Economy

What is emerging across global education markets is a growing structural misalignment. Tuition models in many premium institutions were built during decades of demographic expansion and rising middle-class purchasing power. Today, however, student populations are tightening in many developed economies while household income growth has slowed relative to tuition inflation. At the same time, capital continues to pursue expansion strategies through acquisitions and international market entry. The result is an unusual tension: institutions attempting to scale supply while the affordability foundation that once supported demand is becoming less predictable. In economic terms, the education sector is transitioning from a demand-expansion environment to a competition-for-share environment—a shift that requires far greater discipline in pricing, portfolio strategy, and revenue governance.

Capital Markets Are Becoming More Selective

These pressures are increasingly intersecting with capital market expectations.

Investors who once rewarded rapid expansion are now placing greater emphasis on predictable revenue, disciplined pricing strategies, and sustainable margins.

“In expansion periods, demographic growth masked many operational inefficiencies,” Cohen said.

“In tighter markets, those inefficiencies become visible very quickly.”

Revenue Governance Becomes the Strategic Advantage

Cohen has directed multinational revenue systems within education enterprises operating across more than twenty-five countries, overseeing revenue strategy, enrollment operations, marketing, and technology teams.

Her work has included revenue forecasting tied to demographic modeling, pricing architecture redesign, acquisition diligence, and institutional portfolio strategy.

Under tightening conditions she implemented structural changes that reduced tuition discount exposure, improved net tuition yield, rationalized underperforming programs, and converted previously non-performing initiatives into recurring revenue streams.

“These were not simply enrollment gains,” Cohen said. “They were structural protections for long-term financial stability.”

According to Cohen, institutions that succeed in the next phase of global education will treat revenue as a governed system aligned with demographic and economic realities.

“The era of passive enrollment is over,” she said.

“In competitive markets, precision replaces optimism.”

Media Contact

Education Without Borders

info@edwb.org

https://edwb.org

About Elaina Cohen

Elaina Cohen is a global education strategist specializing in enrollment systems, revenue governance, and institutional growth strategy across multinational education enterprises. Her work focuses on aligning demographic trends, economic conditions, and operational strategy to build resilient education institutions in evolving global markets.

Media Contact

Organization: Education Without Borders

Contact Person: Elaine Jackson

Website: http://www.edwb.org/

Email: Send Email

Country:United States

Release id:42746

The post Pac-Man and Lazy Fatalism: Why Global Education’s Acquisition Frenzy Is Colliding With Economic Reality appeared first on King Newswire. This content is provided by a third-party source.. King Newswire makes no warranties or representations in connection with it. King Newswire is a press release distribution agency and does not endorse or verify the claims made in this release. If you have any complaints or copyright concerns related to this article, please contact the company listed in the ‘Media Contact’ section

Disclaimer: The views, suggestions, and opinions expressed here are the sole responsibility of the experts. No bigeconomymarket.com journalist was involved in the writing and production of this article.